In Q1, rates within the U.S. truckload market finally saw a sustained push upwards — that trend has continued into the second quarter.

Though the overall demand picture remains muted in an uncertain economic backdrop, sustained pressure on the supply side of the market (carriers) has created a tight environment for shippers.

As we dive deeper into the busy summer shipping months, will we continue to see a shift upwards in truckload market rates?

Should shippers be preparing for a very different freight environment by the end of 2026?

We’ll tell you everything you need to know in the latest truckload market guide.

Q2 Truckload Market:

The Complete Guide for Logistics Pros

What you’ll learn in this comprehensive update:

- Q1 2026 truckload market recap

- Macroeconomic outlook

- 7 trucking trends to watch right now

- Q2 2026 truckload market forecast

New to the Curve?

These essential truckload market resources will give you foundational industry knowledge and teach you how how we build our proprietary spot rate index.

Want slides for your next presentation?

Download all the Curve charts and graphs, formatted for slides.

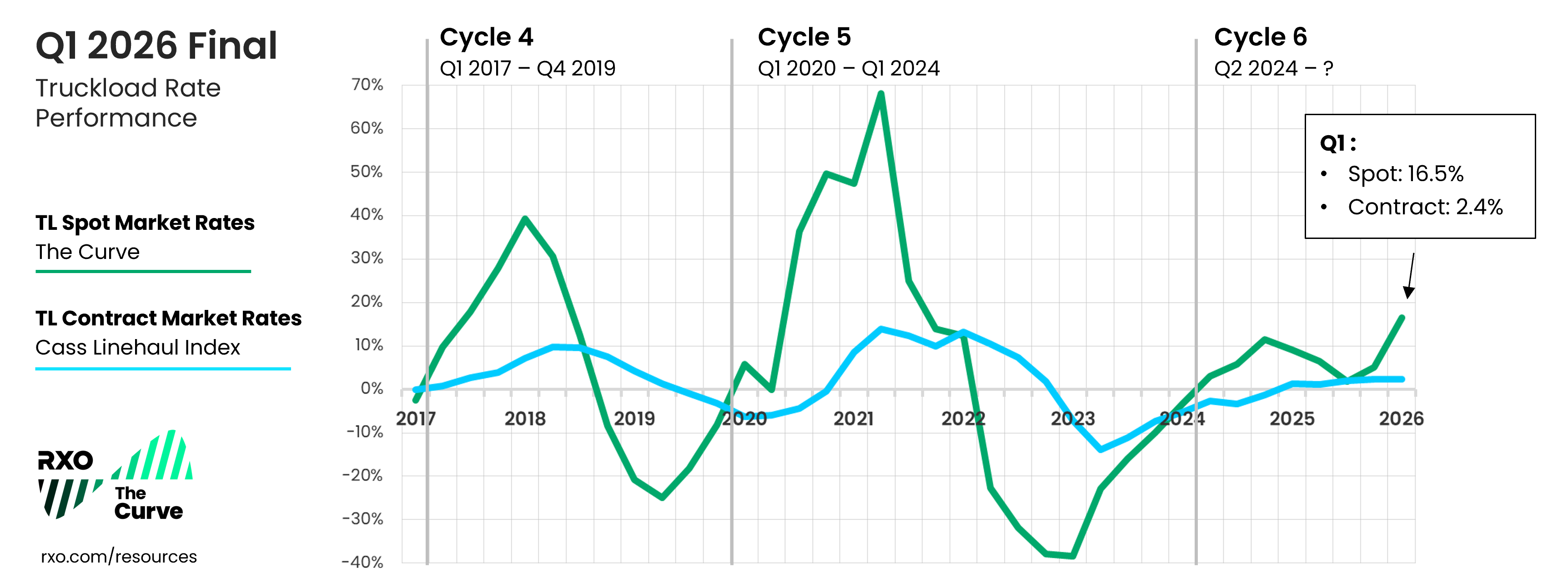

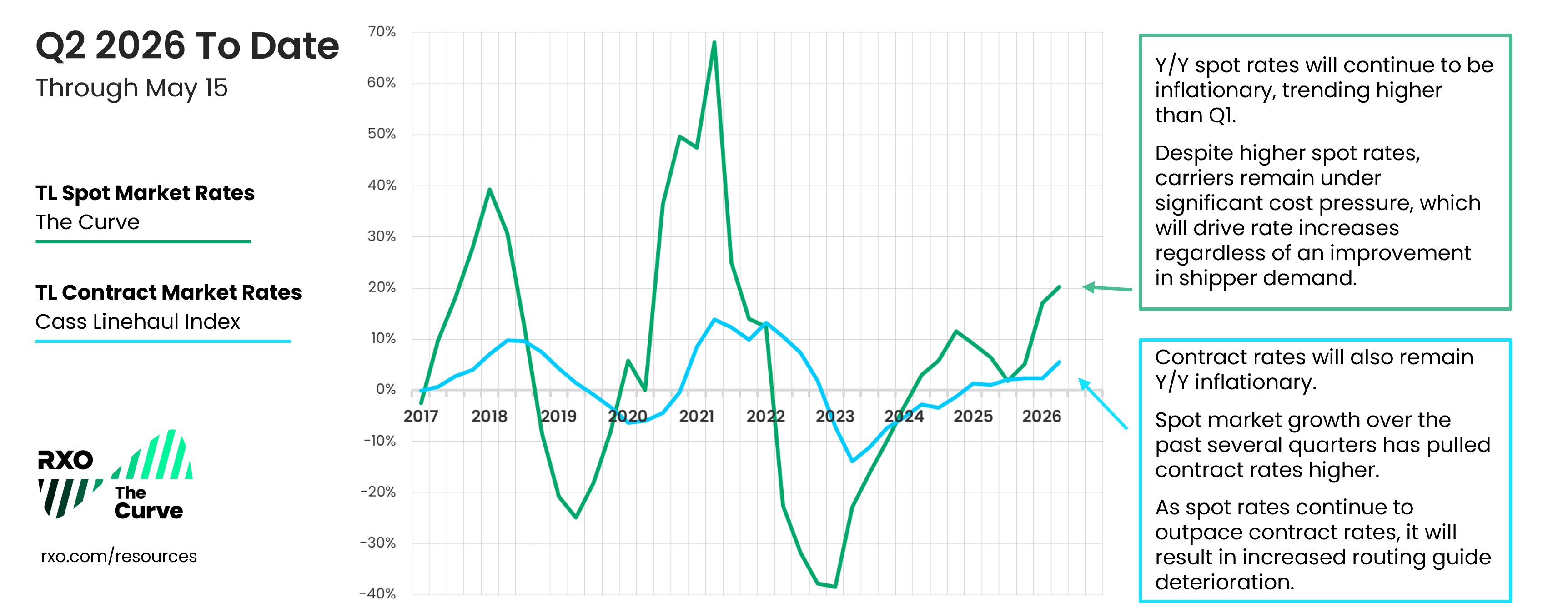

Spot & Contract Trucking Rate Recap: Q1 2025

The RXO Curve index continued to move higher into inflationary territory.

In Q1, the industry experienced continued carrier exits and tight market conditions, which drove spot rate increases.

- Q1 truckload spot rates remained inflationary, up from Q4

Truckload spot rates, (linehaul only, excluding fuel), increased 16.5% year-over-year at the end of Q1, up from 5.2% in Q4. - Q1 truckload contract rates remained inflationary, flat from Q4

Truckload contract rates* increased 2.4% year-over-year, flat from Q4.

Download all the Curve charts for your next presentation.

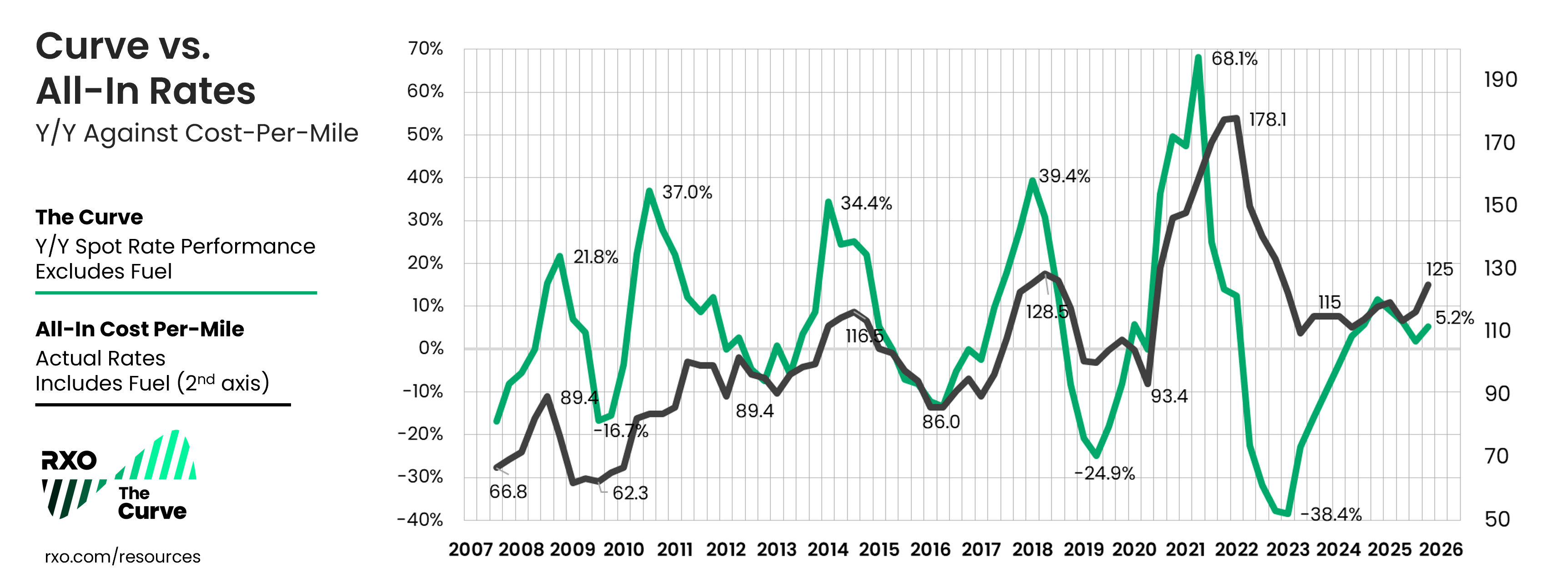

Actual Spot Truckload Rates vs. Year-Over-Year

To build further confidence in the Curve (a year-over-year spot rate index), let’s see it up against our proprietary all-in cost-per-mile index — this is comparing annual change (without fuel) versus the actual rate (all-in cost, with fuel included).

As a reminder, these numbers are informed by real transactional data from thousands of daily shipments over the last 18 years.

From Q3 2023 until Q3 2025, this index was essentially flat, with very little movement, ranging between 111 and 120 (for comparison, during COVID-era shipping in the early parts of the previous truckload market cycle, the index troughed at 93.4 and peaked at 178.1).

In Q4 2025, the all-in index ticked up to 125, the highest reading since Q4 2022.

In Q1 2026, the index went even higher, hitting 129.

Download all the Curve charts for your next presentation.

Q1 2026 Truckload Market: Key Takeaways

- The Curve (measuring year-over-year change in linehaul spot rates, excluding fuel) remained in inflationary territory and increased sequentially in Q1.

- All-in rates (actual amount paid to carriers) increased to their highest level in three .

- Despite improving spot rates, carriers remained under significant cost pressure, exacerbated by higher fuel prices.

State of the Industry: Macroeconomic Overview

Overall, the U.S. macroeconomic environment remains in a similar spot as the last several quarters.

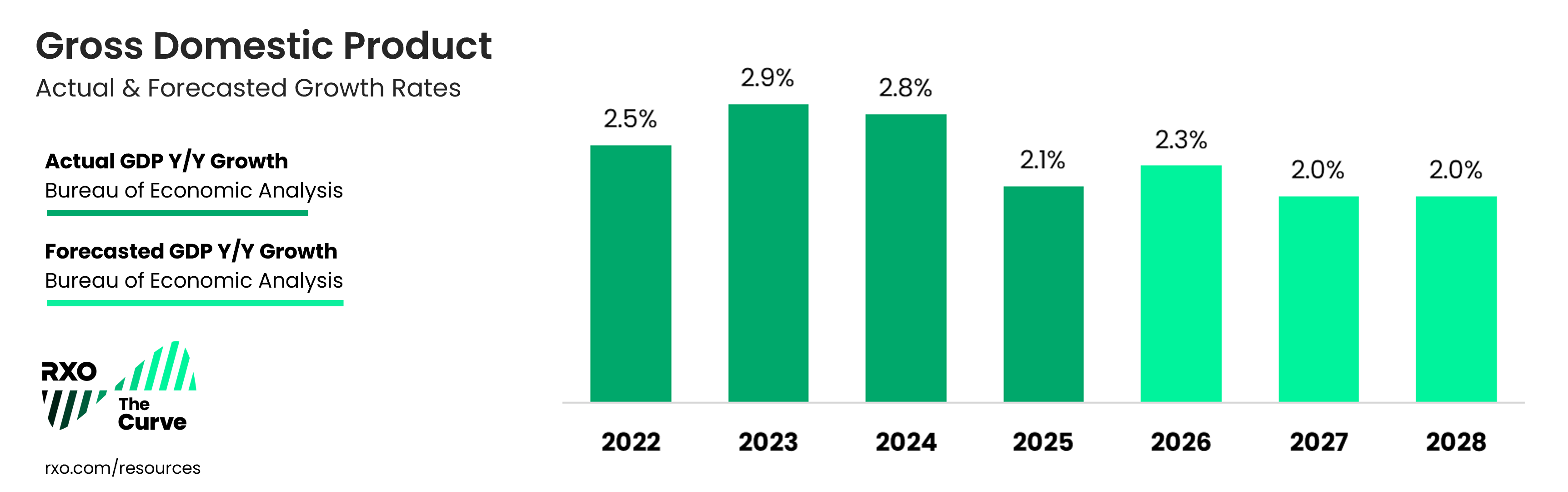

Through Q1, U.S. real gross domestic product (GDP) has remained stable, at 2.7% growth year-over-year.

Though tariffs and trade policy shifts have stabilized compared to earlier in 2025, there is still a looming overhang of uncertainty and consumer anxiety, which has spiked since the U.S. involvement in Iran.

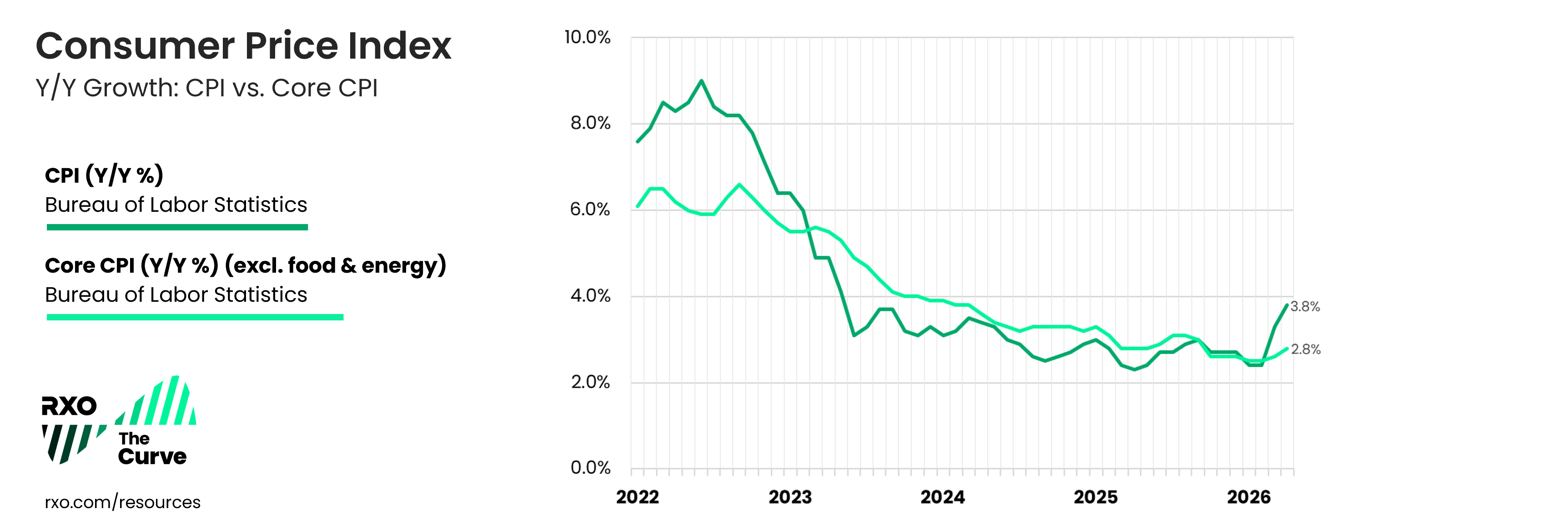

Inflation & Interest Rates

Though inflation has eased considerably over the past three years, it remains persistently higher than the Federal Reserve’s target rate of 2%.

After rising to 3.0% year-over-year in September, the Consumer Price Index (CPI) eased to 2.7% and held steady in October through December, then eased again in January and February 2026 to 2.4%.

However, inflation has reversed course with the start of hostilities between the U.S. and Iran, which has disrupted global oil trade.

In March, the CPI rose to 3.3%, and the core CPI, which excludes volatile food and energy costs, rose slightly to 2.6%.

In April, those figures rose yet again (at an even faster pace than many expected). The CPI rose to 3.8%, with increased energy costs accounting for over 40% of the increase.

Even without fuel, the core CPI still rose to 2.8%.

Tariff and Trade Policy Impact

Throughout 2025, the U.S. government struck several important deals with major trading partners, and the average effective tariff rate for the U.S. has remained effectively flat since May last year.

At this point, most non-tariffed goods (purchased in a flurry of imports early last year) have already worked their way through domestic supply chains.

With shippers now buying imports at higher rates, they must choose between shrinking profitability or passing through increased costs to consumers.

The Supreme Court struck down the Trump Administration’s tariffs — What now?

IEEPA

The legal basis for much of the Administration’s trade policy hinged on the ability to use broad emergency powers to implement tariffs (specifically, the International Emergency Economic Powers Act or IEEPA). In the past, tariffs were generally under the purview of Congress.

Several small businesses and a group of states challenged the legality of these tariffs, which they contended were an overreach of executive branch authority. The case made its way through the lower courts, and reached the U.S. Supreme Court, which had an initial hearing on November 5th.

On February 20th, the Supreme Court ruled that the tariffs exceed the powers given to the president under IEEPA.

Starting in April, the U.S. Customs and Border Protection (CBP) is rolling out a refund process in a phased approach. To claim refunds, importers must file through a newly implemented system,. The CPB estimates they will process refunds within 60 to 90 days of filing.

Alternative Tariff Mechanisms

- Section 122

After the Supreme Court struck down the IEEPA tariffs in February, the administration immediately invoked Section 122 of the Trade Act of 1974 (for unfair trade practices), imposing a 10% surcharge.On May 7, 2026, the Court of International Trade (CIT) ruled that these new tariffs were unlawful. On May 11, 2026, the Department of Justice appealed this decision to the U.S. Court of Appeals for the Federal Circuit and the government was granted a temporary stay of the CIT’s injunction.

It’s important to note that Section 122 Tariffs are temporary by design and can only remain in effect for 150 days (unless Congress passes a specific law to extend them). The Section 122 tariffs that were implemented in February are set to expire in late July 2026.

- Section 301

There are additional tools available to the Administration, notably Section 301 (unfair trade practices) and 232 (national security) tariffs.Section 301 tariffs are similar to Section 122 but have no expiration date. They are also far more complex to implement, requiring lengthy investigations by the Office of the United States Trade Representative (USTR). This is why the Administration used Section 122 tariffs effectively as a bridge until Section 301 tariffs could take effect.

However this shakes out, this could lead to more volatile trade policy and have a significant impact on the economy.

Consumer Confidence

Though the inflationary impact of tariff implementation has been less than originally feared (at least, so far), the U.S. consumer has been leery of how tariffs will impact the economy.

Consumer sentiment (according to the University of Michigan Consumer Sentiment Index) hovered around its lowest ever readings for most of 2025 and even recorded a new all-time low in November.

Though it ticked up slightly in January and February, it has dipped down again with the onset of the war with Iran, dropping to yet another all-time low in April.

Ultimately, inflation and the potential for future interest rate cuts are inextricably linked to changes in both trade policy and geopolitical conflicts, both of which have been highly fluid.

The Federal Reserve and Rate Cuts

After multiple rate cuts in 2024, the Fed sat tight until their September 2025 meeting, where they cut interest rates by 25 basis points (bps). The Fed cut rates by an additional 25 bps in October, and another 25 bps in December.

These cuts brought rates down to their lowest level since 2022.

At its January and March 2026 meetings, the Fed chose to keep rates steady.

Though markets were pricing in one or two more rate cuts in 2026, with the recent rise in inflation (primarily driven by higher oil prices), many think it is unlikely that the Fed will cut rates again this year.

In fact, the market has shifted from expecting rate cuts to now pricing in a possibility of a hike before year-end.

The Fed has a dual mandate of promoting both price stability and maximum employment.

Inflation remains stubbornly higher than the target rate, labor markets are soft (but stable), and the housing market is stagnant.

All that has led to the Fed sitting tight for now.

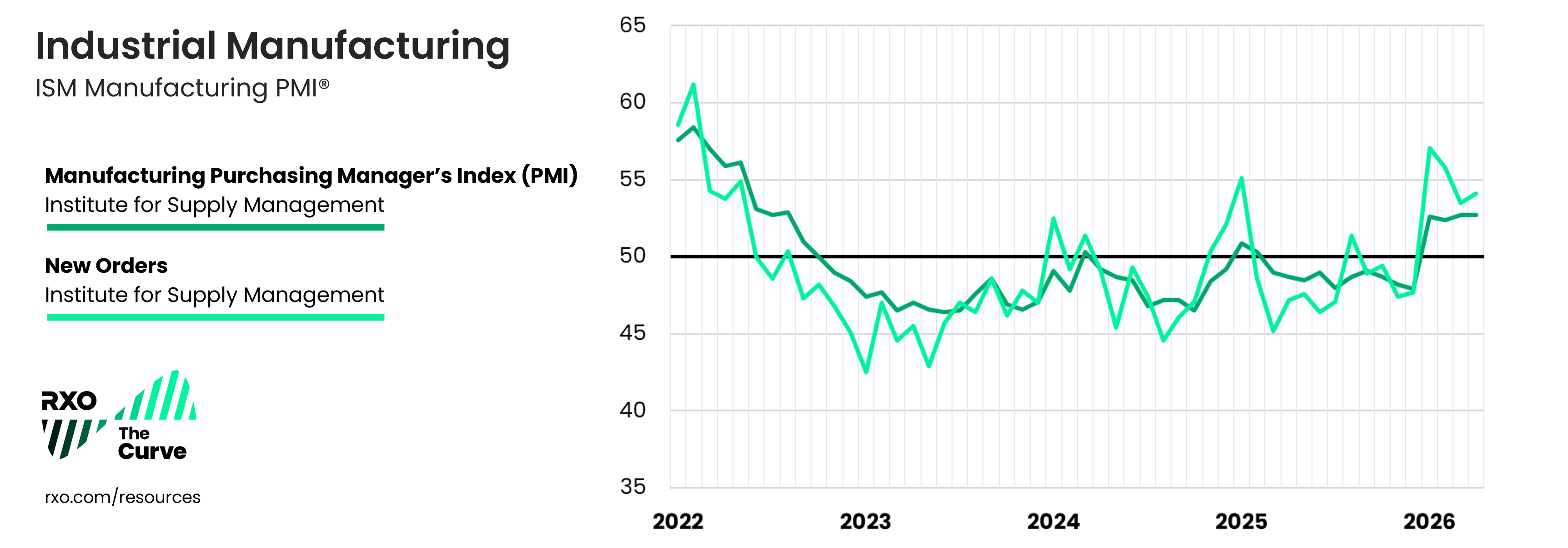

Industrial Demand

After a prolonged contraction, the industrial sector of the U.S. economy was beginning to show signs of improvement in early 2025. The Manufacturing Purchasing Manager’s Index (PMI) entered expansionary territory in January and February of last year, only to sink back into contraction for the rest of the year, primarily due to tariff uncertainty.

In January 2026, however, the index kicked off to a strong start and broke a long period of contraction, jumping into expansionary territory (above 50).

The strength has persisted and the index has been in expansionary territory every month this year. In fact, April marked the longest streak of manufacturing expansion in about 4 years.

Overall, the continued relative strength in the industrial economy is a potential bright spot among lagging consumer prices and rising inflation. This could be partially attributed to the rapidly increasing demand for data center construction.

If industrial demand increases even further, the U.S. trucking economy will see increased freight volumes, which, given the current capacity situation, would mean increased spot rates as well.

Key Economic Demand Indicators Driving the Truckload Market

Now that we’ve covered the broader economy, let’s look at some indicators that are most closely linked to truckload market activity.

Overall, we’ve seen relative stagnation in these indicators (with the exception of imports; more on that below), perpetuating the trend of muted truckload volumes, which have, in turn, slowed down a freight market recovery.

Let’s examine the most recent available figures for industrial production, consumer spending, imports and inventories through the lens of how they are impacting truckload shipping.

Download all the Curve charts for your next presentation.

Note: Truckload Market Inflation/Deflation vs. Economic Growth/Recession

It’s worth noting that though the truckload market is linked to what happens in the wider economy, the two are not always coupled.

Given how supply and demand work in the truckload market, it’s possible for the economy to remain strong and the truckload market to languish. It’s also possible for the truckload market to inflate while the economy weakens (see the inflationary Curve in 2008 during the Great Recession).

More specifically, carriers are combating lagging freight volumes, a continuation of muted spot market rates (until recently) and inflation in their overall cost structures (labor, insurance, etc.).

A continuation of these trends could topple even more carriers who have been barely hanging on for the last two years. More recently, a supply-shock driven by enforcement actions have driven up rates, despite the soft demand environment.

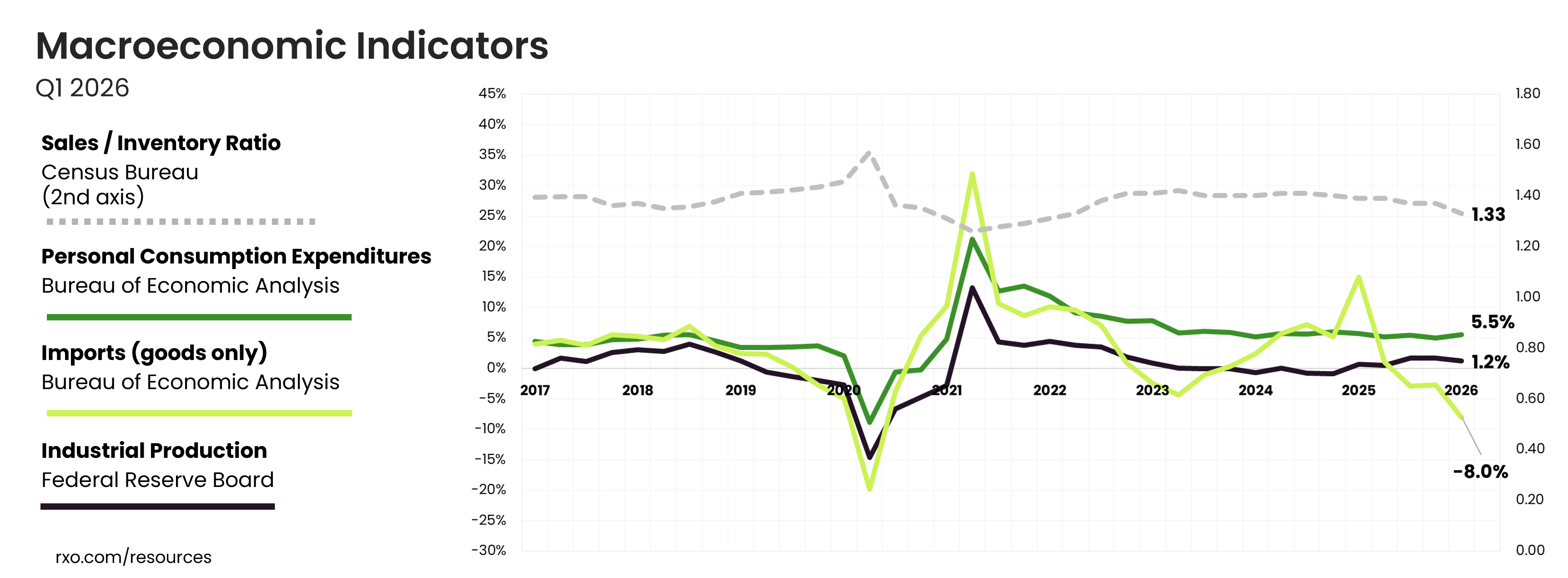

Personal Consumption Expenditures

- What is it?

How much the American consumer is spending - How it impacts truckload shipping:

The more we buy, the more we need to produce (IP) and/or buy elsewhere (imports), which translates to greater demand for truckload shipping.

While we’ve had more than two years of persistent inflation and fears of a possible recession, consumer spending has remained stable, helping to buoy the overall economy.

In Q1, federal tax refunds also likely helped the consumer, who is facing incremental headwinds, including higher gas prices at the pump. The average federal tax refund is up by a low-double-digit percent when compared to the same period in 2025.

This strength is directly linked to the One Big Beautiful Bill Act, which is estimated to have injected approximately $100 billion into higher refunds during this filing season.

Though the consumer spending growth rate has steadily slowed since Q4 2021, returning closer to the historical average, it is still growing; in Q1 the Personal Consumption Expenditures Index is at 5.5% year-over-year, up slightly from Q4 (5.0%).

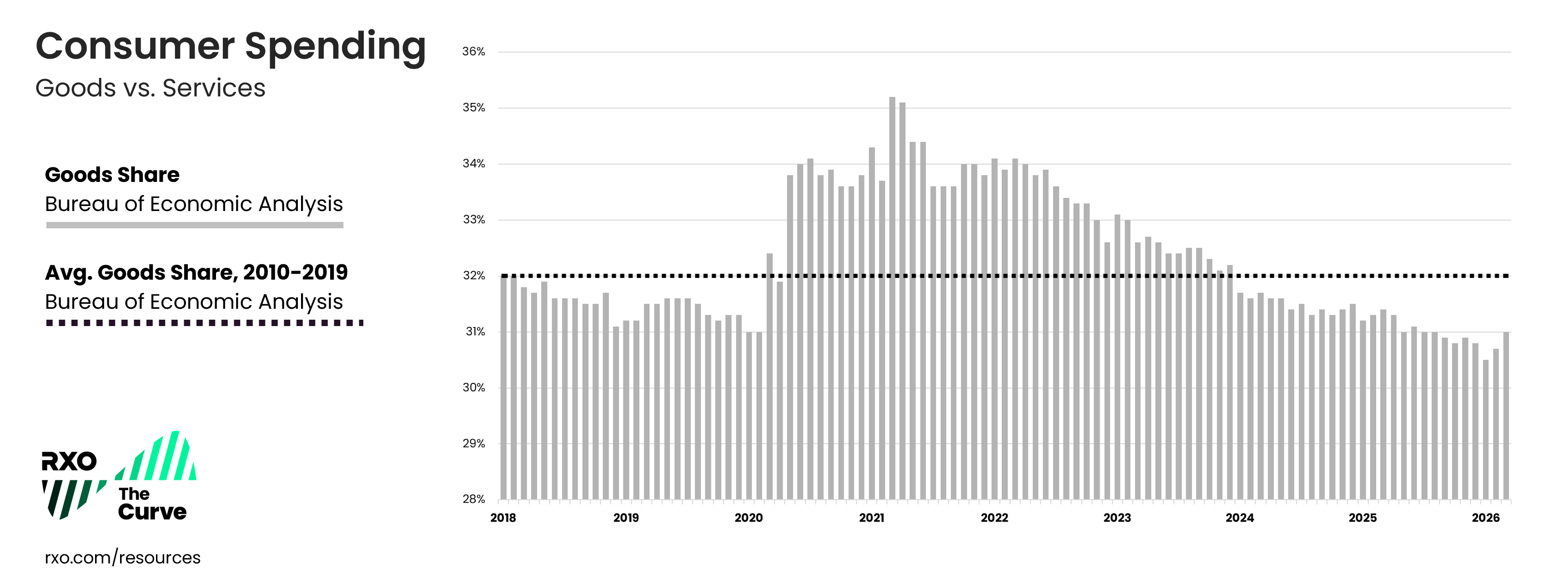

Goods vs. Services in Consumer Spending

When COVID struck, service-related industries closed and, in turn, demand for physical goods (which require more freight shipping) soared to 15-year highs in an incredibly short period of time, driving a commensurately high inflationary spot market.

Over the past several years post-COVID, U.S. consumers have increased their preference for services (vacations, dining, entertainment, etc.), which has decreased physical goods’ share of wallet, resulting in less freight.

Though the rate of decline for total spending on goods has stabilized, it is still tracking below the baseline average (32%) of the 2010s. We’ll look for any increase in this to drive more freight demand in the future.

Industrial Production (IP)

- What is it?

Total value of physical goods America is producing - How it impacts truckload shipping:

The more we make, the more freight that needs to move, from raw material inputs to finished goods

After remaining in slightly negative territory year-over-year for six consecutive quarters, Industrial Production was positive for all of 2025 and finished the year up 1.6% in Q4.

In Q1, IP went slightly downwards to 1.2% year-over-year.

Imports (Goods Only)

- What is it?

Total value of physical goods America is buying from other countries - How it impacts truckload shipping:

The more we buy from other countries, the more freight that needs to move, from raw material inputs to finished goods

After a short-term increase driven by tariffs (many shippers were scrambling to replenish inventories with non-tariffed goods before updated trade policies set in), this index has come back down to earth.

Imports (of goods, excluding services) ended Q4 at -1.7%, declining sharply over the course of 2025.

In Q1 2026, imports dipped even further to -8.0% year-over-year.

Furthermore, continued consumer preference of services over goods could also have a dampening effect on import growth.

Inventory-to-Sales

- What is it?

The ratio of physical goods businesses have in stock vs. how much they’re selling - How it impacts truckload shipping:

When inventory levels are high, it creates a delay in demand for truckload shipping, as businesses will work off excess inventory before producing new goods (IP) or buying more goods (imports).

After peaking at 1.42 in Q2 2023, the inventory-to-sales ratio has gradually trended down, ending Q1 at 1.33.

In fact, the ratio has decreased for the past five consecutive months, with March (latest available) ending at 1.32; we haven’t seen it that low since April 2022.

With so much economic uncertainty amidst muted consumer demand, shippers have been hesitant to build up big piles of inventory. However, as inventories deplete, shippers could potentially launch meaningful restocking efforts later in the year ahead of peak season.

To the extent that consumer demand improves, supply chain leaders may need to undertake restocking efforts to rebuild inventory levels (which would result in increased truckload demand).

Macroeconomy & the Truckload Market: Key Takeaways

- Despite continued headwinds over the past two years, the U.S. economy has avoided a recession (at least for the time being), buoyed by stable consumer spending.

- We are operating in a fluid environment — trade policy, geopolitical unrest, and higher oil prices are driving significant economic uncertainty, which has led to declining consumer confidence and rising long-term inflation expectations.

- There are a few signs for optimism in 2026, including a potential increase in manufacturing and restocking of inventories.

- The last time the freight cycle went inflationary (2020 – 2021), surging demand drove rate growth. For this inflationary leg, the current macroeconomic outlook still doesn’t support a massive spike in demand — instead, supply-side constraints (carrier attrition) is the driving force.

- That said, any increase in demand, even modest, would drive further supply chain volatility.

Truckload Market Trends to Watch in Q2 2026

Let’s unpack a few of the key trends impacting the market before we dive into the updated Q2 forecast.

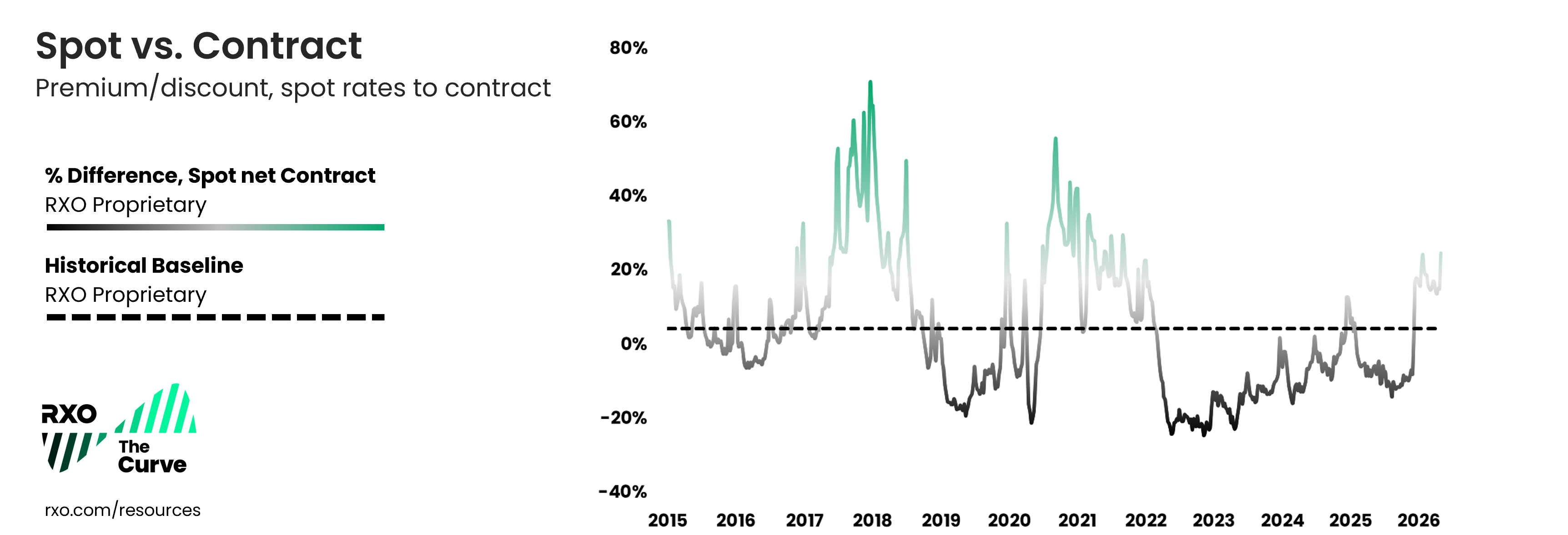

1. Spot rates overtook contract rates — and are holding the advantage.

For the past few years, shippers have used their transportation RFPs as opportunities to bring their contract rates (aka primary rates) back towards pre-pandemic levels — and they were largely successful.

Even though spot rates bounced off the bottom in 2023 and have been year-over-year inflationary since early 2024, they were, in absolute terms, unable to consistently overtake contract rates.

That all changed at the end of 2025, and spot rates have held their advantage throughout Q1 and into Q2, bolstered by immigration enforcement-related capacity attrition and nationwide winter storms.

If this dynamic continues, routing guides will continue to deteriorate as contract rates that were set in the softer market will be pressured.

2. Federal policy enforcement has eliminated carrier capacity.

The federal policy initiative to increase enforcement on non-domiciled CDLs (which is primarily aimed at the immigrant driver population) has significantly impacted the carrier market.

Combined with increased immigration enforcement spending in the One Big Beautiful Bill Act, it has led to a noticeable reduction in the overall driver pool. We expect this to continue in the coming months.

Let’s briefly unpack what’s going on.

Non-Domiciled CDLs

What is a non-domiciled CDL?

In brief, this type of state-issued CDL primarily applies to foreign nationals who are legally in the U.S., but not citizens or permanent residents. Note: This does not apply to Canada and Mexico, whose citizens must obtain their CDL from their home country.

A non-domiciled CDL gives these individuals the opportunity to drive in the for-hire truckload market, provided they complete an application, pass a driving test and provide authorization from U.S. Immigration.

What is happening to non-domiciled CDLs?

The FMCSA issued an interim final rule in late September, that, “Closes gaps in how states issue CLPs and CDLs to individuals from outside of the United States. It tightens eligibility, strengthens safeguards, and makes clear when these licenses must be canceled or revoked, delivering a more secure system and safer roads for all Americans.”

Or to put it simply for our context, it makes it significantly harder (or impossible) for many foreign nationals to drive a commercial vehicle in the U.S.

The FMCSA issued its final rule on February 13, which went into effect on March 16, 2026.

This rule significantly tightens eligibility by requiring specific, vetted employment authorization.

Employment authorization documents alone no longer qualify, and states must verify immigration status through the SAVE system. It also restricts non-domiciled CDLs to certain visa holders.

How much does this affect overall carrier capacity?

The FMCSA estimates that this will push 194,000 drivers out of the market.

The massive and highly fragmented U.S. truckload market is notoriously difficult to quantify, particularly the subsection of the driver population to whom this rule applies (i.e., owner-operators and small fleets), so it’s difficult to say exactly how much this will ultimately impact truckload capacity.

However, it is the biggest structural change to the supply side of the truckload market since trucking deregulation in 1980.

How long will it take for the drivers to exit the industry?

While the final rule gives up to five years before the expiration of relevant CDLs, when combined with ramped up immigration enforcement and English Language Proficiency enforcement, it’s likely that many of the drivers in this population have already opted out of the industry.

Another consideration — insurance companies will be far less likely to extend coverage to carriers that employ non-domiciled CDLs, which would effectively push them out of the market regardless of more direct government enforcement.

3. Carrier employment continues to wane.

As freight volumes and rates have been muted over the past two years, so has driver employment.

Looking at employment data from the Bureau of Labor Statistics (BLS) (which only accounts for W2 employees at fleets, not owner-operators), carrier attrition continues, and we can see drivers exiting the market.

All employees, truck transportation

(from the BLS, through March)

- Decreased sequentially for 34 of the past 38 months

- Decreased year-over-year for 35 consecutive months

Production & non-supervisory employees, long-distance trucking

(aka drivers, from the BLS, through February)

- Decreased sequentially for 29 of the past 38 months

- Decreased year-over-year for 34 consecutive months

4. Though spot rates are helping, carrier profitability remains challenged.

We’ve spent the last several years in a decidedly shippers’ market. With spot rates running hot for the past six months, the pendulum is starting to swing the other way.

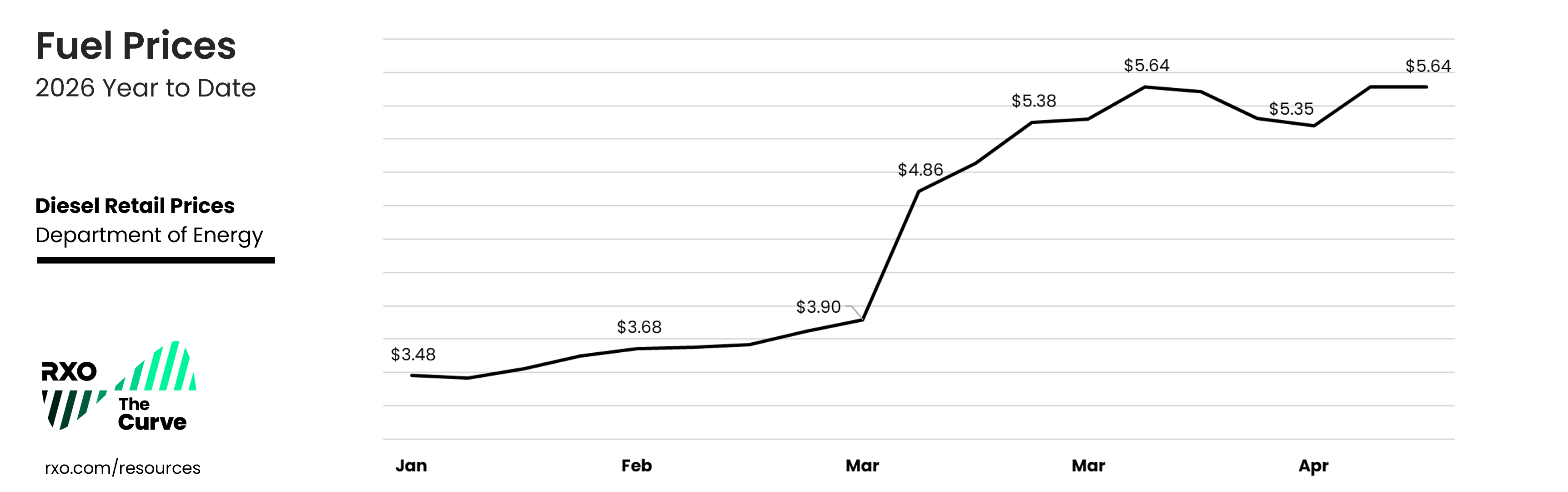

And while carriers are, broadly speaking, in a better position than they were a year ago, trucking companies are facing increasing costs across the board: diesel, insurance, cost of capital, and labor.

Though freight rates may be increasing, there is not currently enough freight volume available to provide the boost that carriers need.

This is especially true for diesel, which has risen 62% since the start of the year.

Though spot freight is generally quoted in real time and with all-in (fuel inclusive) rates, the rate of change in fuel has far outpaced the rate of spot rate inflation.

Widespread routing guide deterioration and even higher spot rates are only being held in check by a muted demand picture.

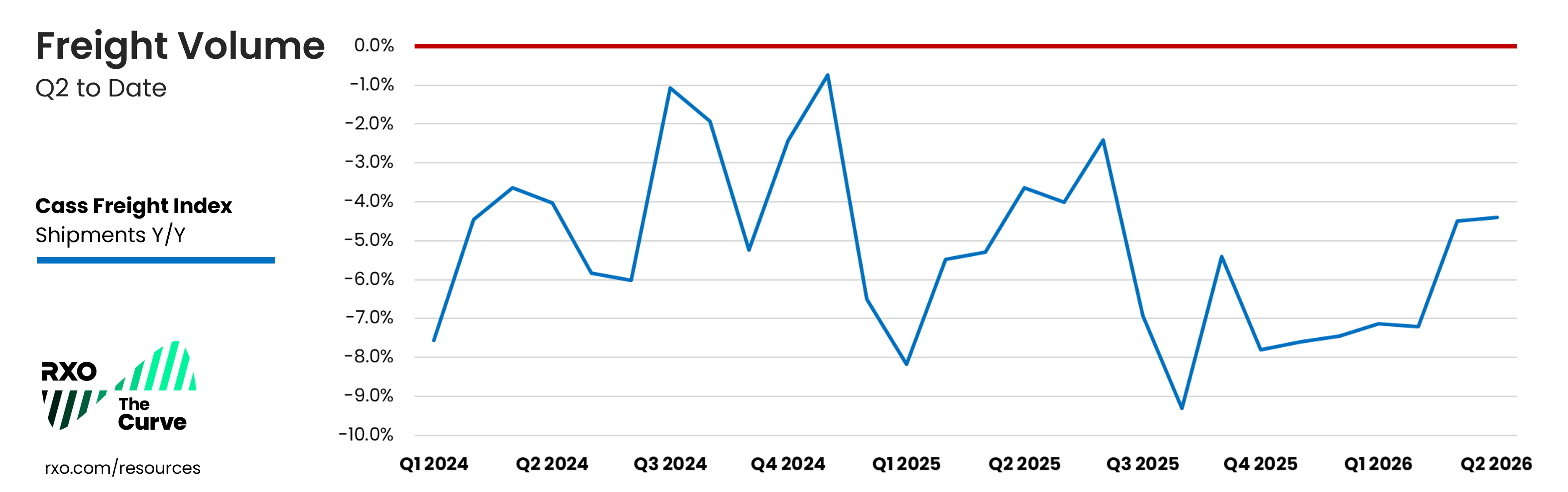

5. Overall freight volumes remain muted.

The Cass Freight Index, which measures truckload shipping volumes, has been year-over-year negative for 14 consecutive quarters.

Though the rate of change has recently slowed (March and April were down around -4.5% year-over-year, compared to down 7% in January and February), it is still in contractionary territory.

For a sustained move higher in freight demand, we would need to see consumers shift away from services back towards goods and a lower interest rate environment.

6. The supply / demand balance is fragile, and susceptible to any volatility.

We’ve outlined the capacity situation in detail (waning employment, decreasing authorities, pressure on the immigrant driver pool, low rates and low freight volumes).

Accelerated carrier attrition over the past year is taking its toll and has set up a more challenging shipper’s market in 2026 with increased rate volatility.

This dynamic was on display during DOT Week in mid-May, which saw week-over-week spot rate increases hit their highest mark in four years. As we approach other summer shipping events, it’s likely that volatility will continue to outpace typical seasonality.

And though demand has been soft, there are some reasons for optimism including recent industrial production data and lean inventory positions.

Any improvement in truckload volume will likely create widespread capacity disruption.

7. Supreme court ruling on brokerage liability.

The Supreme Court of the United States (SCOTUS) delivered a unanimous ruling on May 14 in Montgomery v. Caribe Transport in favor of Montgomery.

The ruling allows brokers to be found liable for negligent hiring of drivers, which was previously preempted by federal law under the Federal Aviation Administration Authorization Act.

This is an evolving situation, but the ruling is likely to have a negative impact on overall carrier capacity, as brokers will be far less likely to use a marginal carrier (i.e., one without a strong safety rating), which will push those carriers out of the industry.

Any further reduction of the available carrier pool would contribute to increased freight rates.

This market backdrop significantly favors scaled, financially stable brokers that have robust carrier onboarding processes and compliance infrastructure. Smaller brokers may not be able to afford increased insurance premiums, and this ruling is likely to accelerate industry consolidation.

If you’re a shipper, make sure you’re using a large, scaled broker with robust carrier onboarding requirements and strong compliance processes.

Truckload Trends: Key Takeaways

- Freight volumes remain sluggish, but spot rates have overtaken contract rates, and this will persist in the months to come.

- Federal policy targeting non-domiciled CDLs and English language proficiency enforcement have significantly tightened the driver market.

- The speed and severity of the upward climb will depend on whether we get an increase in freight demand.

- The capacity situation is much more fragile than at any point since 2022.

Q2 2026 Truckload Market Forecast

We’ve covered the macroeconomic environment, and key trends — but where does it leave us going forward?

We predict the Curve will continue its move into inflationary territory.

We’re in a changing environment, and the carrier market is in a much more precarious place than it has been over the last few years.

Q1 is typically the slowest shipping season of the year, yet industry-wide tender rejections were at their highest levels since 2022 and rate volatility outpaced seasonality.

That trend continues in Q2, and as normal summer shipping seasonality hits, it isn’t likely to slow down anytime soon.

2026 Outlook

Though there has already been a significant impact, we expect carrier capacity to continue leaving the market with the full enforcement of the FMCSA Final Rule on non-domiciled CDLs.

As stated previously, we believe this represents the biggest structural change to the U.S. carrier market since industry deregulation in 1980 — much more than the ELD mandate in 2017.

Though 2025 contract rates slightly increased year-over-year in Q1, spot rates are finally rising at a faster rate. As the gap widens between the two, it will drive volatility as cash-strapped carriers look to increase profitability after a very difficult three years.

If we have a continuation of current capacity trends with an improvement in demand, most shippers’ contract rates will likely not be sustainable.

Q2 2026 Forecast: Key Takeaways

- We are in a shifting market, and the busiest shipping season of the year is approaching.

- The Curve index will remain in year-over-year inflationary territory and finish Q2 higher than Q1.

- A continued increase in carrier exits driven by enforcement of new government rules and/or an increase in freight demand would drive the market even higher into inflation.

- Though both the U.S. consumer and shippers may be hesitant, there are some reasons for optimism including recent industrial production data and government stimulus actions.

- We’re already in a fragile shipping environment, and any increase in demand will drive rates and volatility even higher.

Next Steps: Get Your KPIs in Order With the Research

Did you know that 99% of carriers take shippers KPI expectations into account before agreeing to move a load with them?

As we head deeper into an inflationary market, it’s the perfect time to check yours up against industry standards.

The latest edition of our original, independent research study on logistics KPIs is loaded with insights and benchmarks, informed by 1,000 shippers and carriers.

Check out the research study now to start having a more data-driven network.